2 The Basic Financial Statements

FINANCIAL STATEMENTS: THE “FINANCIAL STORY”

Financial statements help managers answer a variety of questions:

- What and how much does the organization own? What and how much does it owe? Does this organization have enough financial resources to cover its obligations as they come due?

- What are the major sources of revenue for this organization? What are its spending priorities? Do the organization’s sources of revenue and spending priorities reflect the organization’s core mission?

- How much of this organization’s spending does it control? How much of its spending is directed by outside stakeholders like donors, clients, residents, or investors?

- How much, if any, does this organization report in “reserves” or its “rainy day fund”? Given its operations, what would be the optimal level of reserves?

In November 2013, the Contra Costa County (California) Board of Supervisors voted to end nearly $2 million in contracts with the non-profit Mental Health Consumer Concerns (MHCC). The reason: MHCC’s savings account had grown too large.

Since the late 1970s, MHCC has offered patient rights advocacy, life skills coaching, anger management classes, and several other mental health-related services to its poorest residents of the Bay Area. Much of its work was funded through contracts with local governments.

In 2007, its Board of Trustees began to divert 10-15 percent of all money received on every government contract to a reserve account (or rainy-day fund). MHCC’s management concluded that this policy was necessary after several governments were consistently late on their payments. MHCC’s plan was designed to guarantee that the organization would not be exposed to unpredictable cash inflows. The board and management considered this a prudent use of public dollars and a necessary step to protect the organization’s financial future. Beginning in 2007 through 2011, nearly $400,000 flowed into the new rainy-day fund.

Contra Costa County disagreed. They interpreted the contracts to mean reimbursements were only for actual service delivery expenses. They also pointed out that those contracts prohibited carrying over funds from year to year. A reserve fund containing County funds was, therefore, a violation of those contracts. MHCC pointed out that they disclosed the reserve fund strategy in their annual financial reports. The reserve allowed them to deliver services uninterrupted, even during the worst moments of the Great Recession. Contra Costa County Supervisor Karen Mitchoff responded by saying MHCC’s financial statements were not the appropriate channel to communicate such a contentious policy choice. She added, “I am not sympathetic to the establishment of the reserve, and the non-profit board knows they had a fiduciary responsibility to be on top of this.”

The contracts were canceled, and MHCC dissolved in early 2011.

This episode illustrates two of the key takeaways from this chapter. First, an organization’s financial statements are a vital communication tool. They tell us about its mission, priorities, and service delivery strategy. In this case, MHCC made a policy decision to deliver less service in the near term in exchange for the ability to deliver more consistent and predictable services in the future. That choice is reflected in MHCC’s financial statements (e.g., assets exceed liabilities, and unrestricted net assets were a significant proportion of net assets). MHCC disclosed the rainy-day fund policy in the notes to its financial statements. Second, and more importantly, financial statements are only useful if the audience knows how to read them. In this case, Contra Costa County failed to understand how the rainy-day fund policy was communicated in the financial statements and how it affected MHCC’s finances and its ability to accomplish its mission. Without the ability or desire to interpret the financial statements, the County considered MHCC’s actions a breach of contract. Whether a rainy-day fund is, a direct service expense is an important policy question. So is the question of if and how a government should use financial statements for oversight of its non-profit contractors. But to engage these and many other questions, one must first understand how a public organization’s financial statements tell its “financial story.”

LEARNING OBJECTIVES

After reading this chapter, you should be able to:

- Identify the fundamental equation of accounting.

- Identify the basic financial statements: balance sheet, income statement, and cash flow statements.

- Recognize key elements in every financial statement, including assets, liabilities, revenues, expenses, change in net assets, change in net position, and change in fund balance.

- Understand what information each statement is designed to convey about an organization.

BUDGETING VS. ACCOUNTING

If you want to know how an organization connects its money to its mission, read its budget. If the budget calls for more spending in one program and less in another, that tells us a lot about that organization’s priorities. If one of its programs operates at a loss – but another program’s profits subsidize that loss – that is also a clear statement about how that organization carries out its mission. We can think of many other ways an organization’s money does or does not connect to its mission. A public organization’s budget lays out the many unique ways it makes those connections.

But sometimes, we want an “apples-to-apples” comparison. Sometimes we want to know to what extent an organization’s mission-money nexus is the same or different from similar organizations. Sometimes we want to know how efficiently an organization accomplishes its mission compared to its peers. Sometimes we want to know if an organization is in comparatively good or bad financial health. To answer these types of questions, you need information found only in financial statements. In this chapter, we walk through the basic financial statements and the essential concepts from accounting you need to understand in order to interpret the information presented in those statements.

We may need to compare an organization’s finances to the finances of other organizations. If our organization’s expenses exceeded revenues, we might consider that to be a failure – unless, of course, we see organizations like it face similar challenges. If it failed to invest in its capital equipment, we might think it was neglecting its service delivery capacity – unless we saw other organizations make that same trade-off. These comparisons demand financial information based on standardized financial information from a broadly shared set of assumptions. As you’ll see in Chapters 5 and 6, budgets rarely present information in a standard format.

Fortunately, we can get that information from an organization’s financial statements. Financial statements are the main “output” or “deliverable” from the organization’s accounting function. Accounting is the process of recording, classifying, and summarizing economic events in a process that leads to the preparation of financial statements. Unlike budgets, the numbers reported in financial statements are based on generally accepted accounting principles (GAAP) that prescribe when and how an organization should acknowledge economic activity.

GAAP tells us when an organization can say it owns an asset or earned revenue for delivering a service. These are known as principles of accounting recognition. The key point is that GAAP is a shared set of “rules of the game” for summarizing and reporting an organization’s financial activities. If an organization offers GAAP-compliant financial information, we can compare its finances to itself over time and to other organizations.

Standardized rules are not the only difference between budgeting and accounting. Broadly speaking, if budgeting is the story, then accounting is the scorecard. An organization’s budget tells us the activities it wants to do, how it plans to pay for those activities, and what it hopes to achieve. Politicians and non-profit board members love to talk about budgets because budgets are full of aspirations. Budgets are how leaders translate their dreams for the organization into a compelling story about what might happen.

Financial statements tell us what happened. Did the organization’s revenues exceed its expenses? Did it pay for goods and services it received with cash or on credit? Did its investments gain value or lose value? How much revenue would it need to pay for capital improvements and equipment? Accountants often see themselves as the enforcers of accountability. That is why budget-makers and accountants often don’t see eye-to-eye.

These two worldviews are different in many other important ways. As mentioned, budgeting is prospective (i.e., about the future), whereas accounting is retrospective (i.e., focused on the past). Budgets are designed primarily for an internal audience – elected officials, board members, department heads, program managers, etc. In contrast, accounting procedures produce financial reports mostly for an external audience, including taxpayers, investors, regulators, and funders. Budgeting focuses on resources that flow in and out of an organization, also known as the financial resources focus. Accounting focuses on the long-term resources the organization controls and its long-term spending commitments, also known as the economic resources focus. In preparing a budget, the focus is on revenues and spending. In accounting, the focus is on assets and any claims against those assets. We present a summary of these perspectives in the table below.

HOW’S BUDGETING DIFFERENT FROM ACCOUNTING? |

||

|---|---|---|

Characteristic |

Budgeting |

Accounting |

| Metaphor | “The Story” | “The Scorecard” |

| Viewpoint | Prospective | Retrospective |

| Format | Idiosyncratic / Customized | Standardized |

| Audience | Internal | External |

| Focus of Analysis | Inputs / Outcomes | Solvency/Financial Health |

| Organizing Equation | Planned Revenues = Planned Spending | Assets = Liabilities + Net Assets |

| Measurement Focus | Financial Resources | Economic Resources |

| Cost Measurement | Market Price | Historical Cost |

WHO MAKES ACCOUNTING STANDARDS?

The Financial Accounting Standards Board (FASB) produces GAAP for publicly traded companies and non-profits. The Governmental Accounting Standards Board (GASB) produces GAAP for state and local governments. Both the FASB and the GASB are governed by the Financial Accounting Federation (FAF), a non-profit organization headquartered in Norwalk, CT, just outside of New York City. Both Boards are comprised of experts from their respective groups of stakeholders: accounting, auditing, “preparers” (entities that prepare financial statements, like companies and governments), and academia. The Securities and Exchange Commission (SEC), the federal government agency that regulates public companies, designates the FASB as the official source of GAAP for public companies. The GASB has not been designated as such. Still, it is the de facto source of GAAP for governments because key stakeholders like municipal bondholders and credit ratings agencies have endorsed its standards. GAAP for federal government entities is produced by the Federal Accounting Standards Advisory Board (FASAB). The FASAB is comprised of accountants and auditors from federal government agencies. Federal government GAAP is still an emerging set of concepts and practices.

THE FUNDAMENTAL EQUATION OF ACCOUNTING

Everything we do in accounting is organized around the fundamental accounting equation. That equation is

Assets = Liabilities + Net Assets

An asset is anything of value that the organization owns. There are two types of assets: 1) short-term assets, known more generally as current assets, and 2) long-term or non-current assets. A current asset is any asset that the organization will likely sell, use, or convert to cash within a year.

When someone outside the organization owes money, and the organization expects to collect that money within the year, that obligation is known as a receivable. If it’s due within the year, it is classified as a current asset. An organization recognizes an account receivable or A/R when it delivers a service to a client and that client or customer agrees to pay within the current fiscal year. Non-profits frequently report donations receivable or pledges receivable. Pledges receivable represent a donor’s commitment to give at a future date. The same logic applies to grants receivable when foundations or governments commit to giving the organization a grant. Governments recognize an overdue tax payment as taxes receivable. Due from other governmental units represents payments due to a government from other governmental units.

Organizations will report inventory or supplies if they expect to use these resources as they carry out routine operations. These are also current assets.

Most public organizations own buildings, vehicles, equipment, and other assets they use to deliver their services. These are long-term assets, as the organization expects to use them over multiple years (frequently referred to as useful life). Organizations are not likely to sell these assets, as doing so would diminish their capacity to deliver services. State and local governments build and maintain roads, bridges, sewer systems, and other infrastructure assets. These are among the most expensive and essential long-term assets in the public sector.

By contrast, a liability is anything the organization owes to others. To put it in more favorable terms, liabilities are how an organization acquires its assets. Here the short-term (or current) vs. long-term distinction also applies. Current liabilities are liabilities that the organization expects to pay within the next fiscal year. The most common are accounts payable for goods or services the organization has received but not yet paid for and wages payable for services delivered by employees but not yet paid for.

Long-term liabilities are money the organization will pay at some point beyond the current fiscal year. When an organization borrows money and agrees to pay it back over several years, it recognizes a loan payable or bonds payable. Many public sector employees earn a pension while they work for the government, and they expect to collect that pension once they retire. If the government has not set aside enough money to cover those future pension payments, it must report a pension liability (sometimes referenced as net pension liability).

What’s left is called net assets. Technically speaking, net assets represent the difference between assets and liabilities. For private sector entities, this difference is known as the owner’s equity. Public organizations do not have “owners.” Instead, they have stakeholders, or anyone interested, financial or otherwise, in how well the organization achieves its mission. For governments, taxpayers are a rough analog to owners. But unlike shareholders, taxpayers do not have a legal claim to the government’s assets. Their priorities also differ. Taxpayers want to see their governments deliver the services.

Similarly, donors expect contributions to be used to provide services. They do not expect to get their money back if the organization fails. However, they care about the organization’s financial position and frequently focus on whether its operations are sustainable and will continue serving the public for generations to come. For these reasons, net assets are an important part of government and non-profit finances, but they do not have quite the same meaning as owners’ equity for a for-profit entity.

That said, irrespective of sector, we should think of net assets as an indicator of the organization’s financial strength. If its net assets are growing, that suggests its assets are growing faster than its liabilities, and in turn, so is its capacity to deliver services. If its net assets are shrinking, its service-delivery capacity is also shrinking.

We also have to think about the restrictions on net assets. The new accounting rules require non-profits to report net assets “without donor restrictions” and net assets “with donor restrictions.” Prior to FASB Accounting Standards Update 2016-14, net assets reported as unrestricted are now reported as net assets without donor restrictions. Net assets reported as temporarily restricted (i.e., net assets with time or use restrictions) or permanently restricted (i.e., net assets with restrictions that do not expire) are now reported as net assets with donor restrictions. While ASU 2016-14 is a significant change in how non-profits present financial information in their audited financial statements, how they account for these resources in day-to-day operations remains unchanged. Put differently, changes in GAAP do not alter or amend donor intent. Non-profits will need to continue to track gifts – but report in the financial statements in aggregated categories.

Governments use separate classification schemes, but these are a bit more detailed. We describe that scheme later in this chapter.

OWNERS = EQUITY HOLDERS

In for-profit organizations, the fundamental equation is Assets = Liabilities + Owners’ Equity. Conceptually, every shareholder has a claim to assets that do not have an offsetting liability. Put differently, shareholders have a claim to all assets not otherwise promised to creditors or suppliers. When you buy a for-profit company’s stock (or “shares”), you are, in effect, purchasing a portion of that company’s owner’s equity. That’s why stocks are also known as equities. If a company’s assets grow faster than its liabilities, its equity will become more valuable, and the price of its stock will increase, meaning investors who hold that stock make money. If, for example, you had invested in Apple stocks before the first iPod came to market in 2001, as of June 30, 2023, your portfolio’s value would have increased by 58,679 percent (from $0.33 per share to $193.97 per share). The price of Apple shares reflects growth in revenues and, correspondingly, growth in assets.

THE BASIC FINANCIAL STATEMENTS

Organizations that follow GAAP produce three basic financial statements:

- A Balance Sheet summarizes the organization’s assets, liabilities, and net assets at the end of the fiscal period (e.g., as of December 31, 20XX).

- An Income Statement presents a summary of the organization’s revenues, expenses, and changes in net assets for the fiscal year (e.g., for the year ending December 31, 20XX).

- A Cash Flow Statement shows how the organization receives and uses cash to carry out its mission (e.g., for the year ending December 31, 20XX).

In the discussion that follows, you will see more detail about each statement and how the information it contains can inform key management and policy decisions.

When considering an organization’s financial statements, keep one central point in mind: Net assets are the focal point. Regardless of the organization’s structure or mission or changes in assets, liabilities, revenues, expenses, and cash flows will affect net assets. While the content of each financial statement differs, the focus is on net assets.

Additionally, each statement’s presentation style and terminology vary depending on the sector. The table below summarizes these differences.

STATEMENT |

WHAT FOR-PROFITS CALL IT |

WHAT NON-PROFITS CALL IT |

WHAT GOVERNMENTS CALL IT |

||

|

Government-Wide Statements |

Governmental Fund Financial Statements |

Proprietary Fund Financial Statement |

|||

| Balance Sheet | Balance Sheet or Statement of Financial Position | Statement of Financial Positions | Statement of Net Position | Balance Sheet | Statement of Net Position |

| Income Statement | Income Statement, Profit & Loss (P&L) Statement, or Operating Statement | Statement of Activities | Statement of Activities | Statement of Revenues, Expenditures, and Changes in Fund Balances | Statement of Revenues, Expenses, and Changes in Net Position |

| Cash Flow Statement | Cash Flow Statement or Statement of Cash Flows | Statement of Cash Flows | N/A | N/A | Statement of Cash Flows |

Many of the labeling differences are intended to contrast the mission orientation of non-profits and governments with the profit orientation of for-profits. We see this most clearly in the income statement. For-profit organizations often refer to the income statement as the “profit/loss statement,” given that its purpose is to distinguish its profitable products and services from its non-profitable products and services. For governments and non-profits, the focus is on “activities.” The question here is not whether the organization’s activities are profitable but how those activities advance its mission. To be sustainable, every organization must generate more income than it incurs in expenses. That said, profitability is not a primary objective for public sector organizations, as it is in the private sector.

You will also note several differences in what governments call these statements. We have already discussed how financial statements illuminate operational accountability or how efficiently and effectively an organization uses financial resources to advance its mission. Taxpayers want to know that their government delivers services efficiently and effectively. To that end, state and local governments prepare “government-wide” financial statements. These statements present the government’s overall financial position. These statements offer some insights into the government’s ability to continue to deliver services in the future. With a few modifications, these government-wide statements are conceptually like the basic financial statements for a non-profit or for-profit.

The government-wide balance sheet is called the Statement of Net Position, and the government-wide income statement is called the Statement of Activities. By referring to the income statement as the Statement of Activities, standard setters have sent a clear message: governments exist not to generate income but to produce activities. This also explains why there is no government-wide cash flow statement. Information about how a government generates and uses cash does not necessarily help us understand if it is achieving its mission.

But with governments, operational accountability is only part of the story. Taxpayers also want to know if their government did what they told it to do. They want to know if services were delivered with revenues collected. That’s fiscal accountability.

When we think of fiscal accountability in government, we usually think of the budget. A government’s budget is not just a plan – it is the law. Most governments’ constitutions or charters require them to lay out their planned revenues and spending in a special law called an appropriations ordinance. They must pass legislation that makes their budget intentions clear. If they spend more than their budget allows or if monies are spent in ways not specified in their budget ordinance, they are breaking the law.

Budgets are enshrined in law because they are one of our most effective tools to ensure inter-period equity. Inter-period equity is the idea that if a government presents and approves a balanced budget, it is living within its means and not passing costs onto future generations.

Fiscal accountability and inter-period equity are so important that they are built not just into a government’s budget but also its financial statements. For instance, imagine a school district levies a property tax to pay for school buildings. Taxpayers want to see how much revenue that tax generated, how much money the school district borrowed for capital improvements, how much of that revenue is being used to repay those borrowed funds, and so on. They want fiscal accountability on that special tax. To assess this, taxpayers need to see those revenues, expenditures, assets, and liabilities presented separately from all other operations. To do that, the school district must present those finances in a stand-alone special revenue fund.

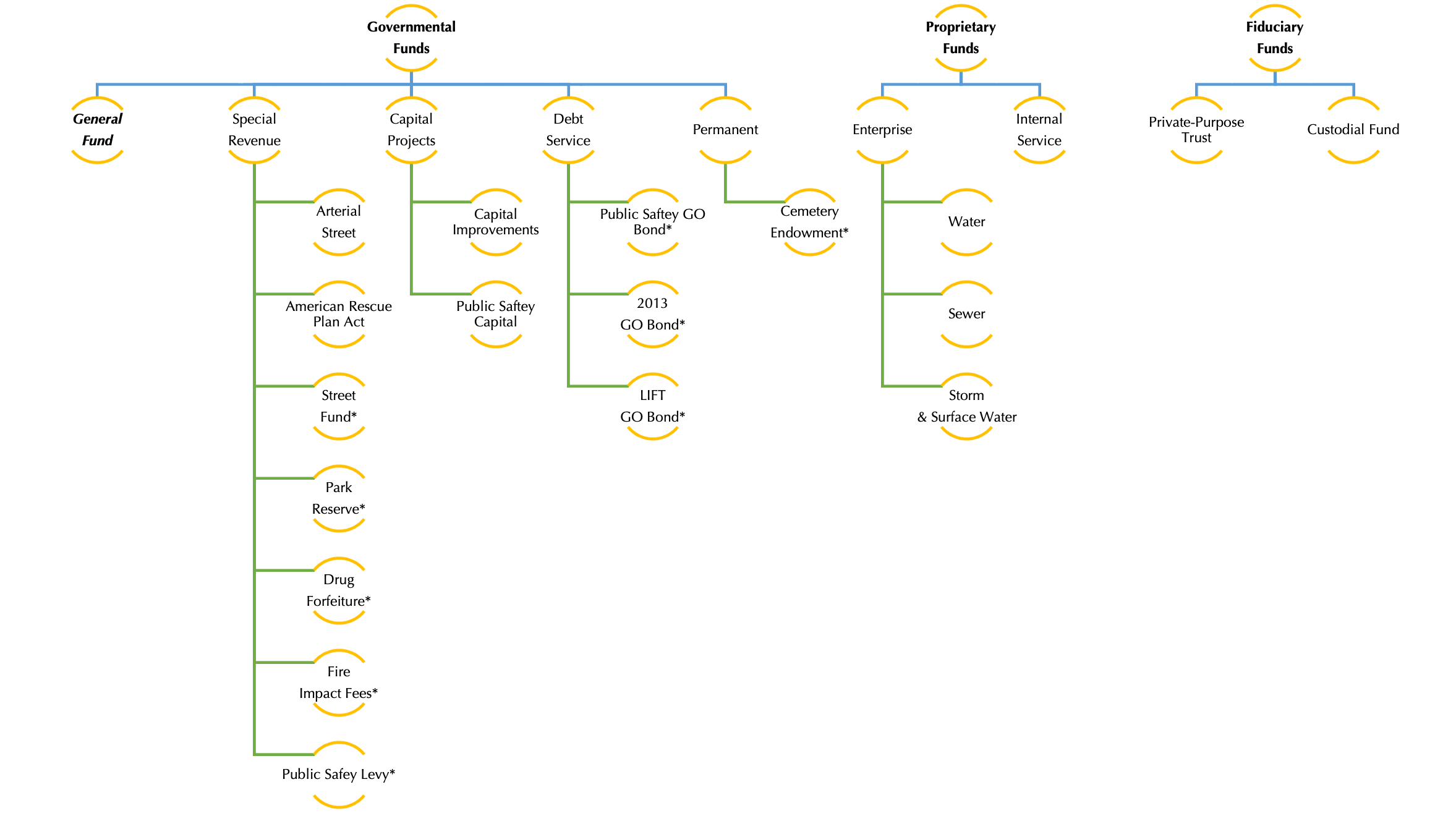

A fund is a stand-alone, self-balancing set of accounts with a specific purpose. The General Fund has every government account for services paid for through general revenue sources. It is where local governments account for police, fire, public health, and other essential services paid for using locally adopted property and sales taxes. It is where state governments account for funding for education (K-12, public universities, and community colleges), public health, public safety, and other essential services paid for using state-wide income and sales tax revenues. For most governments, the General Fund is the largest and most carefully watched. According to GAAP, a government’s General Fund, special revenue funds, debt service funds, capital projects funds, and permanent funds are collectively called governmental funds. The governmental funds account for the government’s core operations and services.

Like budgets, governmental funds focus on near-term revenues and spending (also known as current financial measurement focus). For that reason, the information you see in governmental funds statements is prepared using a different set of accounting principles. Those principles are known as modified accrual accounting (or “fund accounting”). Modified accrual basis of accounting measures the current financial resources available. To that end, revenues are recognized when they are both measurable (i.e., revenues can reasonably be estimated) and available (i.e., revenues are available within 60 days). Expenditures are recognized when the costs have been incurred to acquire goods or services in the current period.

Funds are so important to governments that governments are required to present a separate set of fund financial statements prepared using the modified accrual basis of accounting. The balance sheet in the governmental funds is called the Balance Sheet, and the income statement is called the Statement of Revenues, Expenditures, and Changes in Fund Balance.

Governments also deliver goods and services whose operations are similar to what we would find in the private sector. Examples include water and electric utilities, golf courses, swimming pools, and waste disposal facilities, to name a few. These are known as business-type or proprietary activities. In concept, business-type activities should cover their expenses with the revenue they generate through charges for services. Many governments operate business-type activities because they are profitable and can subsidize other services that cannot pay for themselves. Since business-type activities pay for themselves, we account for them on an accrual basis and prepare a separate set of fund statements referred to as proprietary fund statements. Accrual basis of accounting reports on a transaction when it has an economic impact, regardless of whether it spends or receives cash. Governments reporting business-type activities will prepare a Statement of Net Position, Statement of Revenues, Expenses, and Changes in Net Position, and a Statement of Cash Flows in the proprietary fund statements.

WHAT IS AN AUDIT REPORT?

You will find an audit report at the beginning of every set of financial statements. The report, formatted as a letter prepared by an external financial auditor, is presented to the organization’s board and management and incorporated in the audited financial statements. The auditor performs a series of tests to assess the strength of internal controls (i.e., rules and procedures adopted by an organization to prevent fraud and abuse) and reviews a representative sample of transactions. Their work is designed to answer a simple question: Are the organization’s financial statements a fair presentation of its actual financial position? Usually, the audit report expresses an unqualified opinion, meaning the auditor believes the financial statements are a fair presentation of the organization’s financial position, operations, and cash flows. An unqualified audit report will contain language to the effect of “…these financial statements present, fairly, and in all material respects, this organization’s financial position.” If the auditor has reason to believe the financial statements do not present that position fairly, they will issue a qualified opinion or, in rare cases, an adverse opinion or disclaimer of opinion.

BASIC FINANCIAL STATEMENTS – NON-PROFIT ORGANIZATIONS

The basic financial statements of non-profit organizations include the Statement of Financial Position, Statement of Activities, Statement of Cash Flows, and Statement of Functional Expenses. Below is a quick review of each statement.

THE STATEMENT OF FINANCIAL POSITION

The Statement of Financial Position, the non-profit’s balance sheet, is designed to answer a simple question: What is this organization’s financial position? Financial position has both short-term and long-term components. If current assets exceed current liabilities, then the organization’s short-term financial position is favorable. If long-term (i.e., non-current) assets exceed long-term liabilities, the organization is in a favorable long-term financial position. As you will see in the discussion that follows, an organization could be in a favorable long-term financial position but have a weak short-term financial position, and vice versa.

For that reason, a point of emphasis for the balance sheet is the relationship between the organization’s assets and liabilities. An organization’s net position improves if its assets grow faster than its liabilities. If an organization’s assets decrease or liabilities increase, its net position will deteriorate. We are always mindful of why an organization’s net position has declined over time. Is that because the organization drew down on its reserves during a recession, or do changes reflect a loss in value in the non-profit’s investments? The balance sheet offers a lot of this sort of detail. It also helps organizations formulate strategies to address the issues at hand. If the organization had to draw down on its reserves because of a deficit, it would need to budget for a surplus to replenish reserves. If the organization reported investment losses because of changes in the financial markets, it might opt to do nothing. Doing nothing is a strategy. We’ve seen the markets recover following a recession, including the Great Recession and the COVID-19 recession.

We provide a review of financial health measures, also known as financial statement ratios, that can help you answer some of these questions. Below are some questions you should ask when looking at an organization’s balance sheet:

- Do its total assets exceed its total liabilities? If they do, that is an indicator that the organization’s long-term financial position is favorable.

- Do its current assets exceed its current liabilities? If they do, that is an indicator that the organization’s strong short-term financial position, sometimes referred to as working capital, is favorable.

- Of total assets, what proportion are current assets? What proportion are fixed assets (i.e., buildings and equipment)? What proportion are restricted investments? Buildings and equipment add to operating costs (i.e., maintenance and operating costs). Investments, including restricted (or endowment) investments, are a real source of income, and unrestricted investments may be used to support the organization’s operations.

- Of current assets, what proportion are receivables? What proportion of receivables is due in 12 months or less? What proportion of receivables due is from a single donor or grantor? The concentration of receivables with an individual donor is a source of financial uncertainty.

- What proportion of assets is in the form of cash and cash equivalents? What proportion of current assets is in the form of cash and cash equivalents? How much cash does the organization have relative to its current liabilities? We often hear the phrase cash is king. Cash is a liquid asset that allows the organization to meet its obligations as they come due and provides it with the opportunity to invest in new opportunities or immediately respond to a crisis. At the same time, an organization can have too much cash. If it has more cash than it needs to cover its day-to-day operations, it could invest some of that idle cash in marketable securities or other safe investments and earn a nominal return.

- What proportion of net assets is without donor restrictions? What proportion of net assets is with donor restrictions? Net assets without donor restrictions can be used to cover short-term spending needs, while net assets with donor restrictions cannot, as doing so would violate donor intent.

- Does the organization have non-current liabilities? How might these affect the organization’s current assets in the future? Long-term liabilities like loans, bonds, legal settlements, and pension liabilities increase demand for cash.

It is essential to keep in mind that the balance sheet is a snapshot in time. When an organization’s accounting staff prepares the balance sheet, they present balances in every account on a particular day, usually the last day of the fiscal year. If an organization has a dynamic balance sheet, its financial position could look quite different from one week to the next or one month to the next based on activities in key balance sheet accounts (e.g., cash, accounts receivable, and investments).

Let’s look at an example. The Statement of Financial Position for Treehouse for the year ending June 30, 2022, is below. The financial statements include consolidated accounts of Treehouse and 2100 LLC (i.e., Treehouse’s interest in the 2100 Building) in FY 2022. Treehouse did not include FY 2021 information in its financial statements at the end of FY 2022. That information is presented here for comparison purposes only.

TREEHOUSE |

||

|---|---|---|

CONSOLIDATED STATEMENT OF FINANCIAL POSITION |

||

FY 2022 |

FY 2021 |

|

| CURRENT ASSETS | ||

| Cash and cash equivalents | $4,430,208 | $5,552,763 |

| Investments | $3,162,683 | $4,144,242 |

| Current pledges receivable, net | $970,433 | $35,000 |

| Contributions receivable (rent), net | $195,182 | $582,099 |

| Contracts receivable | $3,528,538 | $1,141,268 |

| Inventories | $315,985 | $393,462 |

| Unemployment trust deposits | $128,572 | $302,309 |

| Prepaid expenses | $364,127 | $46,213 |

| Total Current Assets | $13,095,728 | $12,197,356 |

| LONG-TERM ASSETS | ||

| Long-term portion of pledges receivable, net | $355,448 | $1,308,470 |

| Property and equipment, net | $1,228,420 | 1,227,762 |

| Interest in 2100 Building | $7,097,000 | |

| Endowment investments | $5,189,663 | $6,373,414 |

| Total Long-Term Assets | $13,870,531 | $8,909,646 |

| Total Assets | $26,966,259 | $21,107,002 |

| CURRENT LIABILITIES | ||

| Accounts payable | $143,584 | $286,030 |

| Other liabilities | $266,444 | – |

| Accrued salaries and related costs | $829,883 | $716,656 |

| Total Current Liabilities | $1,239,911 | $1,002,686 |

| NET ASSETS | ||

| Without donor restrictions | $19,743,171 | $12,564,684 |

| With donor restrictions | $5,983,177 | $7,539,632 |

| Total Net Assets | $25,726,348 | $20,104,316 |

| Total Liabilities and Net Assets | $26,966,259 | $21,107,002 |

Download Treehouse Financials: https://bit.ly/3OTmpO7

Every balance sheet will begin with a summary of assets first. Assets are listed in reducing order of liquidity. What that means is that the most liquid asset appears first, and the least liquid assets appear near the bottom. We can convert an asset to cash by selling it or, in the case of receivables, collecting it. Cash is, of course, the most liquid asset. That is why it is listed first. Cash equivalents (including commercial paper and marketable securities like money market mutual funds and overnight repurchase agreements or “Repos”) are safe short-term investments that can be converted to cash immediately at low or no cost. Receivables will convert into cash as clients and donors make payments. Current assets that we do not expect to convert to cash quickly are listed below cash and receivables. Restricted assets are not considered liquid and are reported below the least liquid current asset (e.g., inventory or pre-paid expenses) or are not reported as current assets (e.g., endowment investments).

Treehouse reports the most typical current assets:

- Investments include holdings of stocks, bonds, and other conventional financial instruments, including investments in mutual funds. Note that investments are reported separately from Endowment Investments (non-current), as the latter is subject to internal (board-designated) and external (donor-imposed) restrictions. Note that investments are reported separately from cash equivalents, as they are bought and sold less frequently. This, however, should not be confused with liquidity. A vast majority of financial investments are liquid. However, unlike cash equivalents, investments do not mature every 30 days or every three months; as a result, they need not be actively traded.

- Receivables refer to money owed to the organization. When customers pay money owed to the organization, that asset converts to cash. Treehouse reports net receivables. This means it has subtracted from that receivables figure the portion of those receivables it has determined it cannot collect. Those removals are known as an allowance for uncollectible or bad debt expenses. The nonprofit reports pledges, rent, and contracts receivable separately. Pledges receivable represent a donor’s commitment to give at a future date. Rent receivable represents rent due from tenants in their building. Rent receivable is reported separately from contracts receivable to capture differences in the types of services provided.

- Inventory includes goods that the organization intends to sell or give away as part of delivering its services. Much of Treehouse’s inventory is in “The Treehouse Store,” a thrift store where children can pick up clothing and personal items for free. Many organizations (Treehouse not included) report a separate category for supplies. These are goods and materials, usually commodities, that the organization intends to use while delivering its services. Unlike marketable securities and investments, there may not be a robust market for supplies and inventory, so they are among the least liquid current assets.

- Pre-paid expenses are incurred when an organization opts to pay in advance for services (e.g., insurance, memberships, subscriptions) it will use later. If the organization cancels or renegotiates a pre-paid expense, a refund will be processed for the unused pre-paid amount. This is rare and is subject to contract restrictions.

Treehouse also reports the most common long-term assets. These are listed in decreasing order of liquidity:

- Long-term receivables are monies owed to the organization to be received over multiple financial periods. This is especially true for grants, contracts, and pledges that are not in the current period. These long-term receivables are also reported as net of allowance for uncollectable or bad debt expenses. Long-term receivables must also be discounted to present value using the prevailing market interest rate. Recall that present value is the amount of money a future investment is worth today. Reporting long-term receivables in present value terms recognizes the foregone interest.

- Fixed assets are the least liquid, as the organization’s ability to convert these assets into cash will incur costs and take time. Property and equipment are reported book value – that is, historical cost or purchase price, net of depreciation. Depreciation is the loss in value of an asset due to wear and tear. Effective December 2021, Treehouse became co-owner of its building when a portion of the property was donated to the organization. The Statement of Financial Position reports the fair market value of Treehouse’s share of the building at the time of the donation. Going forward, the value of the organization’s interest will be reported net of depreciation.

BOOK VALUE VS. MARKET VALUE

Accountants usually report assets at historical cost or the cost the organization paid to acquire them. For instance, if an organization purchased a building for $500,000 10 years ago, it would report a book value equal to the historical cost net of depreciation. Meanwhile, an appraiser might estimate that a buyer would be willing to pay $1,000,000 for that building today. This is the building’s estimated market value. Accountants prefer historical costs. In fact, that preference is so strong that it is called the historical cost rule of accounting. Until that building is sold for $1,000,000, that figure is just a guess that is too unreliable as a basis for financial reporting.

- Endowment Investments represent donor-restricted funds. For that reason, endowment investments are frequently listed as non-current assets. Note that investments remain liquid – the classification as a non-current asset reflects restrictions on use. Investment earnings could be invested in the programs or services if donor restrictions do not apply. Treehouse reports endowment investments separately from its other investments and cash holdings. Not all non-profits will report investments this way. That said, they must disclose the different types of endowment funds (or donor-restricted net assets) in the notes to the financial statements.

- Other Investments. Many investments are not liquid because their owner is not allowed to sell them. For example, venture capital funds, hedge funds, and private equity funds mandate lock-in periods. Investors trade off liquidity in these funds but expect higher investment returns. Some investments are less liquid because there are fewer potential buyers. Commercial real estate, for instance, can take some time to sell because there are fewer potential investors interested in those types of properties than in residential real estate. All these investments are reported as “other” long-term assets.

FAIR VALUE VS. HISTORICAL COST

Investments are a notable exception to the historical cost rule. Most investments trade on an exchange like the New York Stock Exchange. The prices quoted in those exchanges are a reasonable estimate of the value of a stock or bond. Since we can readily observe that the fair market value or the value of the investment can be objectively obtained, we replace the historical cost with a fair value estimate. Assuming a non-profit purchased 1,000 shares of Apple stock in 2001 for $0.33 per share, the value of that portfolio, as of June 30, 2023, would have been $193,970. We adjust our books on an annual basis to recognize the gains or losses in the value of our investments. In this case, we would report the change in the investment value as the price of Apple stock increased by $55.86 from $138.11 on July 1, 2022, to $193.97 on June 30, 2023. Despite the considerable gain in the value, accountants are comfortable relaxing the historical cost rule because we objectively measured the value of the Apple stock.

In every balance sheet, liabilities are listed in increasing order of maturity. Maturity refers to the moment in time when payment is due. Said differently, liabilities are listed based on how quickly the organization will need to pay them. Treehouse’s balance sheet includes the two most common current liabilities: accounts payable and accrued salaries and related costs (i.e., wages payable). These are liabilities that will come due within the fiscal year. Like many non-profits, Treehouse does not report any long-term liabilities like a mortgage or a loan. If it had, it would list the proportion due in the next twelve months under current liabilities and the proportion due after that under non-current liabilities.

At a glance, three key features of Treehouse’s balance sheet stand out. First, its current assets far exceed the non-profit’s current liabilities. Its near-term financial position is robust, and the non-profit has more than enough cash to cover its obligations as they come due.

Every balance sheet will present a summary of the organization’s net position (equity, net assets, net position, or fund balance). In the case of Treehouse, a non-profit, its net position is reported in one of two categories: net assets “without donor restrictions” or net assets “with donor restrictions.” Net assets with restrictions include donor-restricted endowment funds (previously listed as permanently restricted) and contributions receivable that are restricted over time and/or use (previously listed as temporarily restricted). Board-designated quasi-endowment funds and accumulated profits are reported under net assets “without donor restrictions.”

The balance sheet shows Treehouse is in a strong financial position, has the right balance across its current and long-term assets, and does not have any long-term liabilities. It also has greater autonomy over its financial resources, as 76 percent of its net assets are not subject to donor restrictions.

NOTES TO THE FINANCIAL STATEMENTS

GAAP imposes uniformity on how public organizations recognize and report their financial activity. But at the same time, all public organizations are a bit different. They have different missions, financial policies, tolerances for financial risk, and so forth. Moreover, large parts of GAAP afford organizations a lot of discretion on how and when to recognize certain types of transactions. For these reasons, numbers in the basic financial statements do not always tell the complete financial story about the organization in question. That is why it is essential to read the “Notes to the Financial Statements.” The notes are narrative explanations at the end of the financial statements. They outline the organization’s key accounting assumptions, share its key financial policies, and explain any unique transactions or other financial activity.

STATEMENT OF ACTIVITIES

The Statement of Activities, the non-profit’s income statement, is designed to tell us if an organization’s programs and services cover its costs. In other words, is this organization profitable?

Every income statement will begin with a summary of revenues and a report of expenses, either by program or line time. In GAAP, revenue is what the organization earns for delivering services or selling goods. Expenses are the cost of doing business. Whenever possible, think of expenses in terms of the revenues they help to generate. For non-profit organizations, this relationship is sometimes clear and sometimes not. For example, imagine that a non-profit conservation organization operates guided backpacking trips. Participants pay a small fee to participate in those trips. To run those trips, the organization will incur expenses like wages paid to the trip guides, supplies, costs related to state permits, and so forth. These are expenses incurred while producing backpacking tour revenue. Here the relationship between revenues and expenses is clear.

This same organization might sell coffee mugs, water bottles, and other merchandise and then use those revenues to support its conservation mission. The expenses to produce those mugs are known as the cost of goods sold. Here again, the revenue-expense relationship is clear. When that link is clear, we can determine if a program/service/product is profitable. That is, does the revenue it generates exceed the expenses it uses up?

In for-profit organizations, profitability and accountability are virtually synonymous. But for public organizations, profitability has little to do with accountability. For instance, our conservation non-profit might accept donations from individuals in support of its conservation work. Which expenses were necessary to “produce” those revenues? The development director’s salary? The administrator’s travel expenses to visit a key donor? The expenses from a recent marketing campaign? Here, the revenue-expense link is less clear. Same for in-kind contributions (i.e., donated goods and services) the organization receives in support of its mission. This link is even murkier for governments, where taxpayers pay income, property, and sales taxes. Those taxes have no direct link to the expenses the government incurs to deliver police, fire, parks, public health, and other services.

To put this in the language of accounting, public organizations have a mix of exchange-like activities, such as backpacking trips and coffee mugs, and non-exchange-like activities, like conservation programs and public safety functions that are just as, if not more, central to their mission as their exchange-like activities. That is why profitability is one of the many criteria we need to apply when thinking about a public organization’s finances.

That said, the main point of emphasis on the income statement is the relationship between revenues and expenses. As mentioned, net assets are a good indication of that relationship. If revenues increase faster than expenses, then net assets increase. If expenses increased faster than revenues, net assets would decrease. The income statement can help illuminate several follow-up questions to understand an organization’s revenues-expenses relationship in some detail:

- How much did net assets increase since last year? How much of that increase was in net assets without donor restrictions? How much was in net assets with donor restrictions? Growth in net assets without donor restrictions indicates that the organization’s core programs and services are profitable. An increase in net assets with donor restrictions can mean many other things. It could mean the non-profit received additional donations that had a time or purpose restriction. The non-profit would need to meet those restrictions over multiple years. It could also mean the non-profit’s endowment reported a positive return. That return may be reinvested in the endowment or diverted to cover core operational expenses.

- What portion of revenue is from earned income versus contributed income? Earned revenue, or revenue generated when the organization sells goods or services, is attractive because managers have direct control of expenses needed to generate that income. Contributions are less predictable and less directly manageable but do not have an immediate offsetting expense – except for fundraising and development costs. That said, the disconnect between donor and beneficiary provides the non-profit with the ability to manage expenses given changes in contributions.

- What percentage of earned revenue is from the organization’s core programs and services? What proportion is from other activities and other lines of business (sometimes known as unrelated business income)? It is common for non-core programs and services to subsidize core programs and services, but is that the right policy for this organization to pursue? Non-profits that generate unrelated business income must pay UBIT – unrelated business income tax on profits earned from activities not substantially related to the charitable organization.

- To what extent does this organization rely on in-kind contributions? Investment income? In-kind contributions will vary by type of organization. Food banks are more likely to report in-kind contributions as a major source of revenue. Treehouse received an in-kind donation of an interest in their building. Professionals in legal, marketing, and accounting service industries frequently provide local non-profits with services for free or at steep discounts. These are reported as in-kind donations.

How much the non-profit reports as investment income largely depends on the size of the investment portfolio. Foundations, for example, will report investment income as the single largest source of revenue. In contrast, for most non-profits, investment income makes up a smaller portion of overall revenues. Still, it often allows the organization to report a surplus at the end of the fiscal year.

To illustrate, let us examine Treehouse’s Statement of Activities for the year ending June 30, 2022. The income statement reports revenues by source and by restriction and expenses by function (program, management, or fundraising). While Treehouse does not report expenses for each program, a detailed list of expenses can be found in the Statement of Functional Expenses.

TREEHOUSE |

||||||

|---|---|---|---|---|---|---|

CONSOLIDATED STATEMENT OF ACTIVITIES |

||||||

Without donor restrictions |

FY 2022 With donor restrictions |

Total |

Without donor restrictions |

FY 2021 With donor restrictions |

Total |

|

| OPERATING REVENUE | ||||||

| Contributions and grants | $9,400,113 | $640,000 | $10,040,113 | $8,257,401 | $350,000 | $8,607,401 |

| In-kind contributions | $662,156 | – | $662,156 | $580.307 | $271,968 | $852,275 |

| Contract revenue | $12,659,996 | – | $12,659,996 | $3,867,313 | – | $3,867,313 |

| SBA PPP proceeds | – | – | – | – | – | $137,164 |

| Other revenue | $23,358 | – | $23,358 | $137,164 | – | – |

| Net assets released from restrictions | $1,270,202 | ($1,270,202) | – | $878,350 | ($878,350) | – |

| Total revenue | $24,015,825 | ($630,202) | $23,385,623 | $13,720,535 | ($256,382) | $13,464,153 |

| OPERATING EXPENSES | ||||||

| Program services | $19,577,929 | $19,577,929 | $8,129,972 | $8,129,972 | ||

| Management and general | $1,659,555 | $1,659,555 | $945,581 | $945,581 | ||

| Fundraising | $2,262,043 | $2,262,043 | $1,588,136 | $1,588,136 | ||

| Total expenses | $23,499,527 | – | $23,499,527 | $10,663,689 | – | $10,663,689 |

| CHANGES IN OPERATING NET ASSETS | $516,298 | ($630,202) | ($113,904) | $3,056,846 | ($256,382) | $2,800,464 |

| NON-OPERATING ACTIVITY | ||||||

| Investment income (loss) | ($505,340) | ($856,252) | ($1,361,592) | $127,859 | $1,246,119 | $1,373,978 |

| Donation of interest in building | 7,097,000 | – | $7,097,000 | |||

| Property related revenues | $123,011 | – | $123,011 | |||

| Property related expenses | ($122,486) | – | ($122,486) | |||

| Total non-operating activity | $6,592,185 | ($856,252) | $5,735,933 | $127,859 | $1,246,119 | $1,373,978 |

| TOTAL CHANGE IN NET ASSETS | $7,108,483 | ($1,486,454) | $5,622,029 | $3,184,705 | $989,737 | $4,174,442 |

| NET ASSETS, beginning of year | $12,634,688 | $7,469,631 | $20,104,316 | $9,379,979 | $6,549,895 | $15,929,874 |

| NET ASSETS, end of year | $19,743,171 | $5,983,177 | $25,726,345 | $12,564,684 | $7,539,632 | $20,104,316 |

Download Treehouse Financials: https://bit.ly/3OTmpO7

For FY 2022, Treehouse reported $23.4 million in revenues. Of that, $10.04 million was from contributions and grants, $0.7 million was from in-kind contributions, and $12.7 million from contract revenue. Most of Treehouse’s income is not subject to donor restrictions (i.e., without donor restrictions). Investment income, classified as non-operating revenues, is reported separately from operating revenues (i.e., grants, contributions, and contract revenue). Investment income would be classified as operating revenue in instances where the non-profit has invested a substantial proportion of its resources to generate income to support core programs or cover overhead costs. That is not the case for Treehouse.

Net assets released from restrictions represent a reclassification of net assets. That reclassification will appear as a reduction in net assets “with donor restrictions” and a corresponding increase in net assets “without donor restrictions.” In doing so, the non-profit is reporting it has satisfied the intent of the donation or grant received in the current or prior period. Remember, restrictions only apply to revenues; they do not apply to expenses, hence the need to release assets from restrictions.

In the expense part of the Statement, we see that expenses for program services were $19.6 million – approximately 83 percent of total expenses. Treehouse reports non-operating income separately from operating income, which indicates that income generated from investments and other sources was not derived from core activities. Not surprisingly, Treehouse reported investment losses at the end of FY 2022 ($1.4 million). It also reported the in-kind donation of an interest in the building ($7.1 million) as non-operating activity. In doing so, the organization conveys to stakeholders that it does not view this donation or related activities as part of its core operations.

Change in net assets is a focal point when reviewing the Statement of Activities. In FY 2022, Treehouse reported a positive change in net assets of $5.6 million. Much of this can be attributed to the in-kind donation of interest in a building ($7.1 million). Adjusting for the gift, Treehouse reported a deficit at the end of FY 2022. However, that deficit was primarily driven by investment losses – not the nonprofit’s core operations. Judging an organization’s performance using data from a single year is often difficult. Five years of data could provide a more compelling narrative of the organization’s financial position and operating results. More on this in Chapter 3.

WHAT IS THE OPTIMAL LEVEL OF RESERVES?

Well, as one of us likes to say, it depends on a wide variety of factors, including revenue mix and volatility, timing of cash flows, changes in demand for services – particularly in an economic downturn – existing capital investments, and the need for capital improvements, to name a few. In creating reserves, a clear statement of purpose, size, and strategy to accumulate, expend, and replenish reserves should be discussed and adopted.

The Non-profit Finance Fund (NFF, see https://nff.org/fundamental/kinds-capital) recommends that non-profits create and accumulate reserves with specific goals in mind. Categories include (a) working capital reserves to ensure timely payment of obligations as they come due, (b) operating reserves used to absorb unforeseen revenue losses or unexpected extraordinary expenses, (c) risk and opportunity capital to support program development and innovation, (d) change capital that helps the organization address strategic issues including social justice, changes in government policies, or existential threats to operations (e.g., disruptive technology), (e) recovery capital to help recover from damaging financial shortfalls, reduce debt, or fund much-needed repairs to facilities and equipment, (f) facilities and equipment capital that finances the purchase of capital equipment or upgrades to existing infrastructure, and (g) endowments that generate investment income that can be used to support core programs or replenish reserves. Organizations need not establish each reserve, and one could argue that the categories are fluid. For example, some could consider operating reserves the same as recovery capital. Others are not. For example, working capital reserves allow the organization to cover program costs while payments from funders are pending. Working capital reserves are essential to every organization and are not the same as operating reserves. Every organization needs a working capital reserve, but not all organizations need recovery capital; therefore, the context of operations and environmental factors matter in creating and drawing on reserves.

How do you build and replenish reserves? Non-profits should budget for reserves. To ensure they meet that goal, they should include budget reserves as a line item in their operating budget or intentionally budget for a surplus. Capital campaigns would raise funds to fund capital improvements or create endowments. However, doing so could divert donations from operating activities. For that reason, the use of capital campaigns to create reserves should be strategic. Governments adopt similar approaches to build and replenish their “rainy-day” or “budget-stabilization funds.” More on this in Chapter 6.

STATEMENT OF CASH FLOWS

The Statement of Cash Flows is just as the title suggests. It tells us how an organization receives and uses cash.

It might seem strange to devote an entire financial statement to a specific asset. But cash is not just any asset. Cash is king! For small organizations, especially small non-profits, it is possible to run out of cash. If that happens, nothing about that organization’s mission, clients, or impact on society will matter. Its employees, vendors, and creditors will not take a compelling mission statement as a form of payment. If the organization is out of cash, it is out of business.

To that end, the Statement of Cash Flows is quite useful if we want to answer a few key questions about how a public organization receives and uses cash:

- Did the organization’s core operations generate more cash than they used? If not, why?

- Did the organization depend on cash flow from investing or financing activities to support cash flows necessary for basic operations? How predictable are cash flows from investing and financing activities?

- How much of the organization’s cash is the result of transactions it cannot directly control (e.g., receivables)?

- How much of the organization’s cash flow is related to sales of goods and inventory? How predictable are those sales?

From the cash flow statement, we can learn a lot about the specific ways an organization generates and uses cash. The statement breaks cash flows into three categories: operations, investing activities, and financing activities. Euphemistically, we call this “OIF” (pronounced “oy-f”):

- Cash Flow from Operations presents a summary of how the organization receives cash and uses cash for its core activities. Negative cash flow from operations indicates that the organization’s basic operations use more cash than they produce. It could mean the organization reported profits because of growth in revenues – but those revenues remain uncollected and are reported as receivables. It could also be the case that the non-profit did not report a profit but reports positive cash flows from operations as a result of collecting outstanding receivables. While our discussion is focused on profitability, keep in mind that without positive cash flows from operations, the organization’s finances are not sustainable.

- Cash Flow from Investing Activities. In this case, investing includes investments in financial instruments or fixed assets like property and equipment. For most non-profits, this section is focused on cash earned from investments. If those investments produced more cash than what was spent to acquire them, they provide positive cash flow. Purchases of buildings and equipment are a cash outflow, and if the organization sells any buildings or equipment, the receipts from those sales also appear here as a cash inflow (though this is rare). In general, we expect positive cash flow from investing activities. It’s essential, however, to know the origins of that positive cash flow. If the organization sold a building, that might produce positive cash flow, but at the expense of its ability to deliver services in the future. It might see negative cash flow from investing activities if, for instance, it moves idle cash into short-term investments.

- Cash Flow from Financing Activities. Financing activities capture any cash the organization borrows to finance its operations. Most of the activity in this section has to do with borrowed money. For-profit entities use this section of the cash flow statement to show how issuing stock produces a cash inflow. For non-profits and governments, the cash inflow from issuing bonds or taking out a loan will appear here. For non-profits with an endowment or other permanently restricted net assets that produce unrestricted investment income, that cash flow will also appear here.

Like with the balance sheet and income statement, net assets are a key part of most public organizations’ cash flow statements, especially cash flows from operating activities. It might seem strange that net assets are the point of departure for a statement about cash, but it makes sense if we are willing to make a few assumptions.

Recall that the most common way for net assets to increase is for revenues to exceed expenses. To understand the cash flow statement, take this idea a step further. Assume that a public organization’s total cash will increase during a fiscal period if the cash inflows from its main operating revenues exceed the cash it pays out to cover its main operating expenses. The “cash flow from operations” part of the cash flow statement is based on precisely this idea. It starts with the assumption that an organization’s change in net assets is a good indicator of its cash flows from operations.

TREEHOUSE |

|

|---|---|

CONSOLIDATED STATEMENT OF CASH FLOWS, YEAR ENDED JUNE 30, 2022 |

|

| CASH FLOWS FROM OPERATING ACTIVITIES | |

| Change in net assets | $5,622,029 |

| Adjustments to reconcile change in net assets to net cash flows from operating activities | |

| Depreciation | $286,275 |

| Donated investments | ($336,936) |

| Net realized and unrealized losses (gains) on investments | $1,568,107 |

| Changes in allowance and discounts on receivables | ($24,422) |

| Donation of interest in building | ($7,097,000) |

| Changes in operating assets and liabilities | |

| Pledges receivable | $42,101 |

| Contribution receivable for rent | $386,917 |

| Contracts & other receivable | ($2,387,270) |

| Inventories | $77,477 |

| Deposits held in trust | $173,737 |

| Prepaid expenses | ($317,914) |

| Accounts payable | 123,999 |

| Accrued salaries and related costs | $113,229 |

| Net cash used in operating activities | ($1,769.671) |

| CASH FLOWS USED IN INVESTING ACTIVITIES | |

| Purchase of investments | ($195,512) |

| Proceeds from sale of investments | $1,129,561 |

| Purchase of furniture and equipment | ($286,933) |

| Net cash investing activities | $647,116 |

| NET CHANGE IN CASH AND CASH EQUIVALENTS | ($1,122,555) |

| CASH AND CASH EQUIVALENTS, beginning of year | $5,552,763 |

| CASH AND CASH EQUIVALENTS, end of year | $4,430,208 |

Download Treehouse Financials: https://bit.ly/3OTmpO7

Most sizable public organizations follow this concept and report their cash flows from operations using the indirect method. This method starts with the Change in Net Assets, assuming that change is the result of cash flows from operations. But of course, not all changes in net assets are the result of positive or negative cash flow. Different transactions and accounting procedures can affect revenues or expenses without affecting cash flow. A typical example is depreciation. Depreciation is when an organization “uses up” some portion of an asset to deliver services. The portion of that asset’s value that is used up is recorded as a depreciation expense. Like all expenses, depreciation reduces net assets. But at the same time, there is no cash flow associated with depreciation. You will not find checks written to an entity called “Depreciation.” The same is true for changes in the value of an organization’s investments. Its stocks, bonds, and other investments can increase in value, but unless it sells those investments, that increase in value will not produce any positive cash flow. Depreciation and changes in the value of investments are both examples of reconciliations. These are transactions that affect net assets but do not involve a cash flow.

In FY 2022, Treehouse produced its Statement of Cash Flows using the indirect method. Treehouse reported a positive change in net assets or surplus at the end of FY 2022 ($5.6 million). Using the Statement of Cash Flows, we want to understand how core operations contributed to the nonprofit’s operating position ($5.6 million) and whether that operating position resulted in higher cash balances. Skip down to the row “Net cash flows from operating activities,” and you will see that in FY 2022, Treehouse’s operating activities resulted in a net cash outflow of $1.8 million. In other words, while the nonprofit reported a large surplus, that surplus did not result in an increase in cash. In fact, core operations resulted in a $1.77 million decrease in cash balances.

To appreciate these differences, review the reconciliations reported under “Adjustments to reconcile change in net assets to net cash flows from operating activities.” Recall that the figures in this part of the statement are reconciliations, so we interpret them inversely. Any activity that decreases net assets is shown here as a positive value because we are “adding back” those activities to arrive at Net Cash Flows from Operations. Any activity that would increase net assets is shown as a negative value (or in parentheses) because we are “backing out” those activities to arrive at Net Cash Flows from Operations.

Treehouse reported several reconciliations in FY 2022. Treehouse reported $286,275 in depreciation expense. Depreciation expenses decrease net assets. We add back deprecation to the Change in Net Assets to arrive at Net Cash Flows from Operations – i.e., the estimate of the change in cash flows from operating activities.

Treehouse reported an increase in discounts and allowances for uncollectables of $24,422. That increase in discounts and allowances decreases Change in Net Assets. We reconcile this item by backing out the change in allowances.

Treehouse received $336,936 in donated investments and $7.097 million in donated interest in the 2100 building. These transactions increase net assets (or profitability) but do not produce a positive cash flow. We deduct (or back out) contributed property and investments from Change in Net Assets. The same logic applies to realized and unrealized losses (gains) on investments. Treehouse reported $1,568,107 in investment losses at the end of FY 2022. Since these cash flows are restricted, and all cash flows are reported under investments – not cash – we add (or deduct) back that loss (gain) from Change in Net Assets.

Below the reconciliations, you will see “Change in Operating Assets and Liabilities.” The figures listed here are also reconciliations, this time to reconcile changes in assets and liabilities that do involve cash to Changes in Net Assets. The key here is that we are focused on changes in assets and liabilities as a result of cash flows. So, to make sense of the Change in Operating Assets and Liabilities section, first, think about how typical assets and liabilities interact with cash.

Cash balances are lower if assets other than cash are higher. If, for example, receivables are higher this year compared to the previous year, cash balances will be lower – in other words, the payment we should have received for a donated pledge or services provided has yet to be received. Consider contracts and other receivables. In FY 2022, contracts receivable was $3,528,538. In FY 2021, contracts receivable was $1,141,268. The increase in receivables implies that payments were pending, so our cash balances are $2,387,270 lower. The same logic applies to prepaid expenses, which increased from $46,213 at the end of FY 2021 to $364,127 at the end of FY 2022. The same logic applies when assets other than cash and investments increase. For example, balances in contributions receivable in FY 2022 were $195,182 – $386,917 lower than they were in FY 2021 ($582,099). That reduction resulted in an increase in cash. The same logic applies to inventories and unemployment trust deposits.

CHANGE IN ASSET OF LIABILITY |

NET CHANGE IN CASH & CASH EQUIVALENTS |

| Increase in an asset account | Decrease in Cash & Cash Equivalents |

| Decrease in an asset account | Increase in Cash & Cash Equivalents |

| Increase in a liability account | Increase in Cash & Cash Equivalents |

| Decrease in a liability account | Decrease in Cash & Cash Equivalents |

Cash balances are higher if balances in liability accounts are higher. Given the focus on Net Cash Flows from Operations, we focus here on accounts payable, other liabilities, and accrued salaries and related costs. As we noted earlier, any change in balances of any notes payable or loan payable would be reported in Net Cash Flows from Financing Activities. More on this below.

Consider Accounts payable. In FY 2022, accounts payable were $143,584, nearly half the balance reported at the end of FY 2021 ($286,030). This decrease in payables implies payments were made, as such, cash balances are $142,446 lower. Conversely, balances in other liabilities and accrued salaries and related costs were higher in FY 2022. Delayed payments mean the non-profit holds more cash now, so cash balances are higher ($266,444 and $113,227, respectively).

The Cash Flows from Investing Activities and Cash Flows from Financing Activities sections are more intuitive. Like before, an increase in an asset account reported under Investing Activities (e.g., Investments or Property and Equipment) results in a decrease in cash and cash equivalents and vice versa. An increase in a liability account reported under Financing Activities (e.g., Loan Payable) results in an increase in cash.

Returning to Treehouse, we see that in FY 2022, it purchased $286,933 in furniture and equipment and $195,512 in investments. The nonprofit reported the sale of investments ($1,129,561). The net effect of investing activities was $647,116 – in other words, investing activities (including the sale of investments) increased the cash position of the nonprofit.

Treehouse did not report any Cash Flows from Financing Activities. It did not report any long-term obligations, did not draw on any line of credit, and did not rely on borrowed funds. This reflects the nonprofit’s strong financial position but also the choice of the board to use internal resources to manage its cash position.

We can draw two immediate and important conclusions from Treehouse’s Statement of Cash Flows. First, the non-profit reported a large surplus ($5,622,029). While there were changes in account balances related to the non-profit operating activities, those activities did not generate cash. As a result, net cash flows from operating activities are negative ($1,739,671). The nonprofit relied on proceeds from the sale of investments to improve the organization’s cash position. At the end of FY 2022, the nonprofit’s cash position had declined from $5,552,763 at the start of the year to $4,430,208 at the end of the year. While the cash position has declined, it’s important to contextualize those findings. The nonprofit reported a large surplus because of a significant increase in revenues and the value of donations (investments and interest in building). While the nonprofit does not expect to liquidate the donated space, the contracts and other receivables should be collected in the next 12 months, improving the nonprofit’s cash position.

Statement of Functional Expenses

One of the central questions in non-profit financial management is: How well does this organization accomplish its mission? From a financial standpoint, one way to answer this question is to determine how much of the organization’s expenses are related to its core, mission-related services. In the language of accounting, this distinction is program services vs. support services (i.e., administrative services). According to paragraph 28 of FASB Statement 117, program services are “activities that result in goods and services being distributed to beneficiaries, customers, or members that fulfill the purposes or mission for which the organization exists.” Support services are everything else: fund-raising, communications, management, administrative support, and other activities necessary to deliver program services.

Donors want to support a non-profit’s primary goals. They want to know if their contribution improved a child’s education, fed the hungry, funded scientific research, or advanced objectives outlined in the organization’s mission. They are less interested in funding rent, insurance, professional memberships, administrators’ salaries (gasp!), or other support services. To be clear, support services are essential. They’re just not sexy. That is why one of the most closely watched numbers in non-profit financial management is the program expense ratio, computed as total program service expenses/total expenses. Many donors look for organizations with comparatively high program expense ratios, and many non-profit leaders work hard to minimize their support service expenses for that same reason.

The program services vs. support services distinction is so important that GAAP calls for a fourth basic statement to illustrate it. This statement is called the Statement of Functional Expenses. It shows three basic categories of expenses:

- Program. Many non-profits report their program expenses separately for each of their major mission or programmatic areas.

- Management and General are principally salaries and benefits for administrators, technical support services like accounting and information technology, and reconciliation expenses in areas like depreciation.

- Fundraising includes expenses related to fundraising and special events, identifying and contacting donors, and other expenses associated with soliciting and generating contributions.

TREEHOUSE |

||||||||

|---|---|---|---|---|---|---|---|---|

CONSOLIDATED STATEMENT OF FUNCTIONAL EXPENSES, YEAR ENDED JUNE 30 2022 |

||||||||

PROGRAM SERVICES |

SUPPORT SERVICES |

|||||||

|

Enrichment Programs |

||||||||

|

Education Programs |

Free Store |

Other |

Total Program Services |

Management and General |

Fundraising |

Total Support Services |

Total |

|

| Payroll | $4,395,285 | $314,944 | $3,256,070 | $7,966,299 | $534,943 | $1,489,412 | $2,024,355 | $9,990,654 |

| Payroll taxes and benefits | $1,095,975 | $73,316 | $689,588 | $1,858,879 | $153,356 | $158,137 | $311,493 | $2,170,372 |

| Free store & holiday magic | – | $805,346 | – | $805,346 | – | – | – | $805,346 |

| Assistance to specific individuals | – | – | $5,740,043 | $5,740,043 | – | – | – | $5,740,043 |